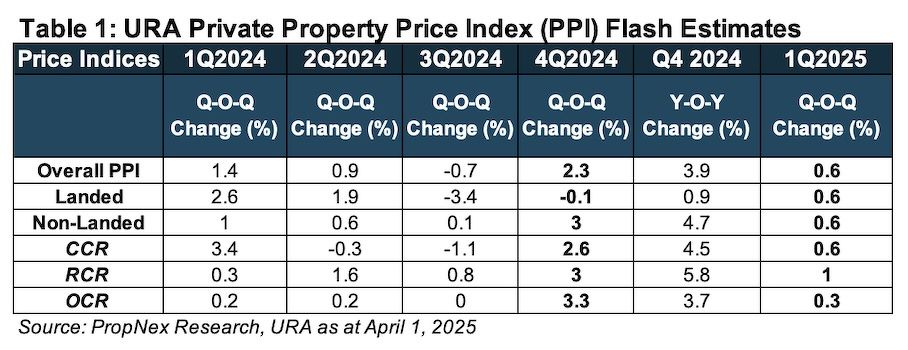

The overall private residential price index in 1Q2025 rose 0.6% q-o-q, according to URA flash estimates on April 1. Price growth eased despite 2025 starting the year with robust new home sales in the first quarter.

Private residential property sales volumes (excluding executive condos or ECs) for 1Q2025 are on track to achieve “a four-year high for a first-quarter sales performance”, says Wong Xian Yang, Cushman & Wakefield head of research for Singapore and Southeast Asia.

Wong attributes the moderated price growth to “high-base effects” following the sharp 4Q2024 spike of 2.3% in private residential prices.

The 0.6% q-o-q increase in private home prices in 1Q2025 was consistent for both landed and non-landed properties. Compared to 4Q2024’s 3% increase, the 0.6% q-o-q growth in 1Q2025 represented a moderation in non-landed property prices. It represented a rebound from the 0.1% dip in 4Q2024 for landed properties.

In 1Q2025, new project launches across all three market segments – Core Central Region (CCR), Rest of Central Region (RCR) and Outside Central Region (OCR) – set benchmark prices in their respective neighbourhoods. However, the price premiums were realistic compared to the secondary market, notes Tricia Song, CBRE head of research for Singapore and Southeast Asia.

Non-landed price growth led by RCR

The price performance across non-landed segments was led by the RCR, which recorded the most significant increase of 1.0% q-o-q, extending its 3.0% q-o-q rise in 4Q2024. The CCR followed, with price growth of 0.6% q-o-q after a 2.6% increase in 4Q024. Comparatively, the OCR grew at a flattish 0.3% q-o-q after a moderate 3.3% growth in 4Q2024.

RCR’s outperformance could have been boosted by the launch of the 777-unit The Orie, the first new launch in Toa Payoh, a mature estate, in nine years – not since Gem Residences in 2016. The Orie sold 668 (86%) of its total units at an average price of $2,704 psf at launch.

In the OCR, new launches Elta in Clementi and Parktown Residence in Tampines set new benchmark prices in their respective neighbourhoods, which have not seen new supply in at least five years, notes CBRE’s Song. Elta sold 65% of its total 501 units at its launch weekend in February 2025, at an average price of $2,537 psf, while Parktown Residence, an integrated development in Tampines North, sold over 87% of its 1,193 units at an average price of $2,360 psf.

Coinciding with the launch of The Orie was Bagnall Haus, the freehold 113-unit project along Upper East Coast Road in the OCR, where over 60% of the units were sold over the first weekend at an average price of $2,490 psf.

The sixth project in Lentor Hills estate, Lentor Central Residence, sold 93.3% of a total of 477 units at an average price of $2,200 psf at its launch weekend. The price achieved is comparable with Lentor projects launched two years ago, points out CBRE.

The four OCR launches (Elta, Parktown Residence, Bagnall Haus and Lentor Central Residence) collectively accounted for 1,922 transactions in 1Q2025, based on caveats lodged as at April 1. New home sales in the OCR (excluding ECs) in 1Q2025 are on track to post the strongest quarterly sales in more than three years, says PropNex.

The CCR saw the launch of Aurea, the 188-unit residential component of Golden Mile Complex’s redevelopment in 1Q2025 (Photo: Samuel Issac Chua/EdgeProp Singapore)

CCR price growth tempered

The CCR saw the launch of Aurea, the 188-unit residential component of Golden Mile Complex’s redevelopment in 1Q2025. A total of 23 units were taken up at the launch weekend at an average price of $3,005 psf.

CCR price growth could have been tempered by discounts offered at existing projects such as the 351-unit One Bernam, which adjusted prices to clear remaining unsold inventory. The project is now 100% sold after 102 units were taken up in 1Q2025 at a median price of $2,523 psf.

On the other hand, some existing CCR projects also achieved slightly higher average prices in 1Q2025 from the previous quarter, including 19 Nassim, 32 Gilstead, Park Nova, and The Collective at One Sophia, according to PropNex Research.

Based on URA Realis data as of April 1, 2025, the price gap between CCR (average price $2,834 psf) and RCR (average price $2,722 psf) is just 4.1%. Between CCR and OCR (average $2,349 psf), it’s just 20.6%.

“On an average unit price psf basis, the price gap between new non-landed private homes sold in the CCR and that of RCR and OCR in Q12025 are at their narrowest in more than 20 years,” says Ismail Gafoor, CEO of PropNex.

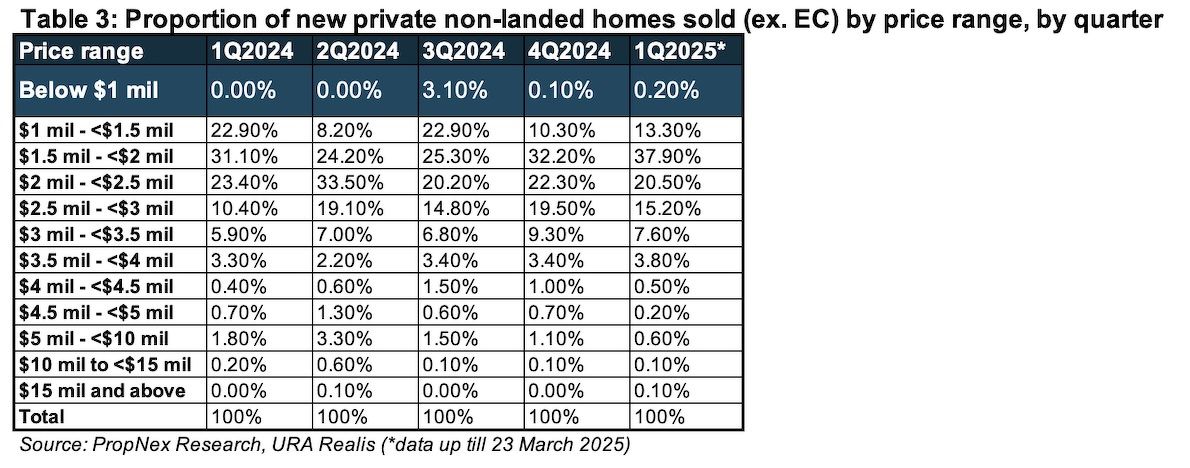

72% of non-landed new homes sold below $2.5 mil

Of the 3,311 non-landed new homes sold in 1Q2025, about 1,705 units were those below $2 million, which is significantly higher than the 1,432 units inked in 4Q2024, says Christine Sun, chief researcher and strategist at OrangeTee Group. Conversely, new non-landed homes sold at higher price tags of at least $3 million dropped to 423 units from 526 units over the same period.

Meanwhile, URA Realis caveat data showed that around 2,800 private homes had changed hands in the resale market in 1Q2025. The resale figure is set to underperform the 3,702 private resale homes that changed hands the previous quarter. “While primary sales held firm on the back of strong take-up at a slew of attractive new launches amid lower interest rates, secondary sales have slowed as buyers gravitated to new launches in 1Q2025,” says CBRE’s Song.

With construction costs still high and land prices still firm, PropNex’s Gafoor anticipates new launch prices will remain resilient. “Price quantum will continue to be a key decision-making factor for homebuyers and investors,” he says.

In 1Q2025, around 72% of non-landed private new homes were sold at prices below $2.5 million, up from 65% in 4Q2024, based on caveats lodged. According to PropNex, the majority of these transactions at below $2.5 million were for units at Parktown Residence, The Orie, Lentor Central Residences, and ELTA.

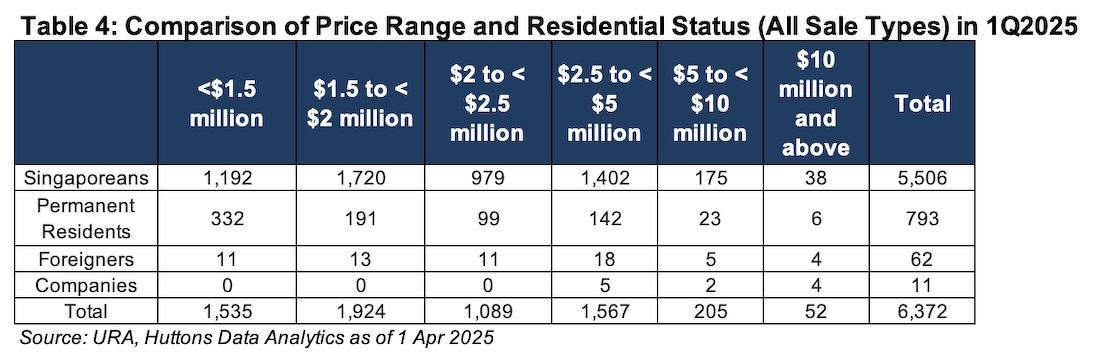

Singaporeans made up 86.4% of new homebuyers

An estimated 86.4% of new home purchases in 1Q2025 were made by Singaporeans, compared with 85.9% in 4Q2024. Permanent Residents (PRs) made up 12.4%, while foreigners accounted for 1.0% of buyers in 1Q2025, according to Huttons Asia data analytics.

With more sales recorded in the OCR in 1Q2025, the proportion of purchases below $2 million increased to 54.3% from 52.4% in 4Q2024. “This is the sweet spot for many OCR projects,” says Lee Sze Teck, senior director of data analytics at Huttons Asia. “These are usually the two-bedroom and some three-bedroom units which fits the demographics of buyers.”

Lee estimates that 8,364 units across 18 projects are slated for launch from 2Q2025 to 4Q2025.

In April, new project launches include 21 Anderson with 18 luxury units (CCR), the 107-unit Arina East Residences (RCR), the 358-unit Bloomsbury Residences (RCR), the 937-unit One Marina Gardens (RCR) and the 638-unit W Residences Singapore – Marina View (CCR) are set to preview.

“While 1Q2025’s new sales have held up, mainly on attractive OCR and RCR projects, most new launches for the rest of 2025 will be in the CCR, which have higher price points and may not generate the same kind of volumes,” says CBRE’s Song. “With most pent-up demand in the suburbs and city fringe realised, pricing and design will be crucial for the upcoming new launches to continue this momentum.”

This version of article first appeared at EdgeProp Singapore.

Photo: Samuel Issac Chua/EdgeProp Singapore